Infrastructure Valuation

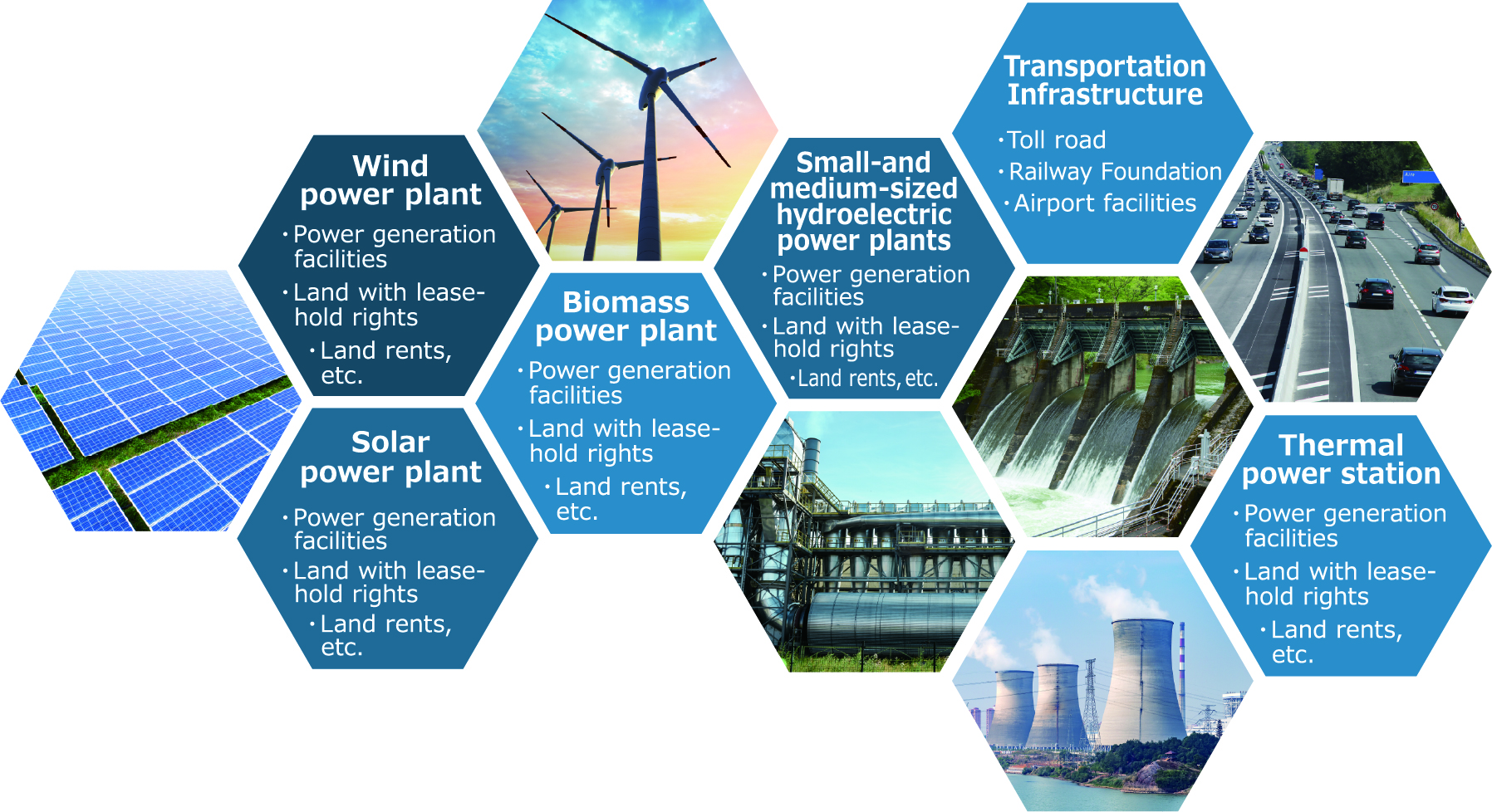

Major Subjects of Valuation

In recent years, the investment market for renewable energy power generation facilities has become active, and a majority of the requests have been made for the valuation of solar power plants.

We can provide valuation reports on high-precision solar power plants, etc., based on enormous revenue and expenditure data.

We also specialize in the valuation of superficies and land with leasehold rights (so-called leased fee interest in land) and the valuation of land rents.

- 2019 Valuation Results

- Solar Photovoltaic Facilities, etc.

/ Output Size:0.5MW to 98MW Total: 470MW

Major clients

For infrastructure valuation, mainly requests from asset managers and operators, sponsored companies such as major electric power companies, real estate companies, securities companies, banks, and local governments.

Valuation standards, etc.

We conduct valuation based on real estate appraisal standards and related considerations, practical guidelines, operational guidelines, and research products.

- Real Estate Appraisal Standards

-

The Real Estate Appraisal Standards were established in 1964 when a real estate appraiser conduced an appraisal of real estate.

This is a uniform standard that serves as a base.When the leased land is regarded as real estate, most of the infrastructure assets are composed of real estate and personal property.

Therefore, the appraisal is conducted by a real estate appraiser based on the real estate appraisal standards.

-

Personal Property Valuation,

including personal property that functions as an integral part of real estate -

This is a research report that was compiled by the Investigative Research Committee of Japan Association of Real Estate Appraisers

(Subcommittee for Review of Real Estate for Business Use).The discussion includes (1) valuation of mortgages by real estate foundations including factory foundations, (2) hotels including personal property, it comprises the valuation of nursing/ healthcare facilities and others, and (3) the valuation of renewable energy power generation facilities using FIT.

License

We have a large number of employees who have obtained the double license of real estate appraiser and ASA certified asset appraiser.

The valuation of infrastructure facilities will be mainly undertaken by the employees who have this double license.

Major Valuation Methods

We determine the final opinion of the value by selecting or using the three methods of cost approach, sales comparison approach, and income approach, in principle.

As a typical example, when a solar power plant is composed of superficies, FIT rights, and equipment, the cost approach and the income approach are applied together.

In this case, the final opinion of the value and its breakdown value (superficies, FIT rights, and equipment) can be presented(*).

(*) In many cases, the breakdown of the final opinion of the value is estimated using the proportion of the value indicated by the cost approach.

- Cost Approach

-

The cost approach to value first determines the reproduction cost of the subject property on the date of the value opinion.

Where the improvement is not a new structure, an estimate of accrued depreciation must be deducted from the reproduction cost.

A value indication determined by this approach is called the value indicated by the cost approach.

- Sales Comparison Approach

-

The sales comparison approach uses data on the sales of comparable properties to determine the subject property’s value.

First, the appraiser gathers a large amount of comparable sales data, from which the most appropriate data are selected.

The market prices negotiated in the comparable sales are adjusted for differences in sales conditions or changes occuring over the passage of time, if required.

Market-specific and property-specific value influences are then compared to get the value indicated by the sales comparison approach.

- Income Approach

-

The income approach estimates the total present value of the adjusted net operating income of net cash flow(NCF) that the subject property is expected to generate in a future period.

The value indication derived from this approach is called the value indicated by the income approach.

There are two basic methods for determining the value indicated by the income approach.

One method, called direct capitalization, applies a capitalization rate directly to net cash flow(NCF); the other method, discounted cash flow (DCF), discounts the net cash flow (NCF) generated over the typical holding period together with the reversionary value at the end of the holding period. Each income stream is discounted to present value at the time it is generated. All the discounted income streams are then added up.